Our goal is to share information and products that are truly helpful to renters.

If you click on a link or buy a product from one of the partners on our site, we get paid a little bit for making the introduction. This means we might feature certain partners sooner, more frequently, or more prominently in our articles, but we’ll always make sure you have a good set of options. This is how we are able to provide you with the content and features for free. Our partners cannot pay us to guarantee favorable reviews of their products or services — and our opinions and advice are our own based on research and input from renters like you. Here is a list of our partners.

Does my roommate need renters insurance?

If you’re a renter and have a roommate you are probably wondering whether or not you need roommate renters insurance. There are a lot of things to consider like; What does your lease say? Does my policy have restrictions on who I can add? Are you married or related? And, should I share my existing renters insurance policy with my roommate?

We answer these questions and more about whether or not your roommate needs renters insurance too.

The basics of roommate renters insurance

Renters insurance will not cover your roommates unless they are related to you or their names are listed in the policy. When determining whether or not you can/should split renters insurance with your roommate there are few basic things you should know.

• Is your roommate a relative or spouse?

Spouses and adult relative roommates are automatically covered under your policy. Policies often have language like, “named insured, resident spouse, and resident relative”. This means they are covered under your policy if you live together.

• Is your roommate on your lease?

Most renters insurance policies require that your roommate be listed on your lease in order to be on the same renters insurance policy. That means if they are subletting, couch surfing, or any other manner of sharing living costs, but aren’t actually on the lease, your roomie must have their own renters insurance policy.

• Did your roommate move in after you already had a renters insurance policy?

Most renters insurance policies require that all adults living in your apartment be listed on your policy in some way even if they are not insured under it. If you get a new roommate be sure to let your renters insurance company know.

The pros and cons to splitting rent insurance with a roommate

Like deciding whether to split anything else with your roommate, there are pros and cons to splitting renters insurance with him or her. While the short-term immediate savings seem great — there are quite a few reasons why being on the same renters insurance policy with your roommate may not make sense.

Pros of splitting rent insurance with your roommate

- Relatives and spouses are already covered

There’s typically no additional expense for relatives and spouses so you’ll both save a bit of money vs. if you insured separately.

- Save money on renters insurance premium

Sharing renters insurance can be a great way to save some money and still have the security of knowing that your stuff is covered. One consideration, however, is that while the average renters insurance policy is about $13 a month for one person, adding a second non-related person will drive the average up to more like $18 a month. So it will cost you less overall, but you may not be saving as much as you think.

- You don’t have to worry about your roommate maintaining coverage

Adding your roommate to your policy helps you ensure you are compliant with the apartment lease — especially if you are worried they might not maintain their coverage without you. Not having coverage if your landlord requires it, violates the lease and could be cause for eviction.

Cons of splitting rent insurance with your roommate

- Missed payments

If your roommate is responsible for making the premium payment and misses it, you might not lose your coverage.

- Any claims filed by your roommate go on your claim history record

Claim history records are maintained for at least three years and filing a claim will possibly increase your renewal premium.

- Your roommate has more expensive items than you

If your roommate has expensive things, that could drive up the cost of your policy resulting in you paying for more than your share. The obvious solution here is to negotiate a split of the bill that is proportionate to your insurance coverage needs.

- Claim payouts

All ‘named insureds’ listed on your renters insurance policy will have their names written on checks for claim payouts. This means that everyone will have to sign the claim payout, which could create problems in certain situations.

- Move a lot

If you move around every year or so it is probably too much of a hassle to bother trying to split renters insurance. Constantly having to work out whose is what, how much each person should have to pay, etc, could get tiresome if you are a bit of a rolling stone.

- Bundling your insurance

If you are bundling your renters insurance with auto, life, or other, it may be difficult to know exactly how much to ask your roommate to contribute for their part of the renters insurance portion of the premium.

Tips for sharing renters insurance with your roommate

1. Make sure you know your roommate

Did you just meet your roommate or have you been friends for a while? Know the person you are splitting financials with to make sure they are reliable.

2. Add renters insurance to your roommate agreement

Having a roommate agreement can save you a ton of headaches. If you do have a roommate agreement and decide to split your renters insurance with them then make sure you add that to your agreement.

Confirm the amount, how you share it, when and how the premium is paid, what happens if you have to make a claim, what happens if one of you needs to move or break the lease early, and anything else you can think of.

3. Document all of your stuff

Whether you take pictures or videos, make sure that you and your roommate’s things are documented so that if something does happen you can get reimbursed. Documenting also confirms who owns what so there is no arguing over what was whose.

4. Talk to your renters insurance company

Look up, call or support chat with your insurance company to make sure you understand your renters insurance policy and confirm how to add your roommate and exactly how much it will cost you.

Why does it cost money to add my roommate to my renters insurance policy?

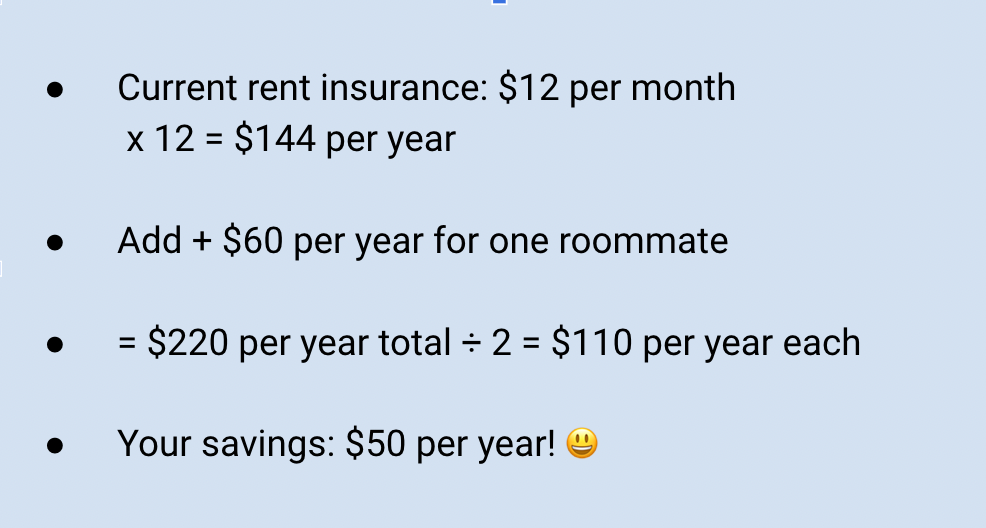

Adding a roommate means adding costs. Your roommate has things and they become an added liability which means the insurance company is taking on added risk. The average added cost runs around $60 annually, which, when you do the math still works out cheaper than having your own coverage (not to mention the rent savings).

Example:

If you are looking into a company like Lemonade, adding your spouse is free, and adding a significant other (that you are not married to) is only an extra $1.67 a month. BUT, they do not allow you to add your roommate to your policy. He or she needs to get her own. So it’s important to check to see if your renters insurance company even lets you add roommates.

How do I share renters insurance premiums with a roommate?

Most roommates split their renters insurance premium 50-50. Renters insurance for an apartment is generally under $20 per month to cover all of you and your roommate’s stuff. Just remember that each roommate needs to be named on the insurance to receive benefits.

If one of you needs extra coverage for expensive items like jewelry or music equipment, you will most likely need an added rider to your policy. If this is the case then that person should pay the additional amount.

It’s usually best to pay the entire premium for the year so that you don’t have to worry about one more monthly payment to keep track of. You will also find that paying your premium annually will save you some extra cash.

What are some other ways that I can save on my roommate renters insurance premium?

There are a ton of ways to save on your renters insurance. Maintaining good credit, bundling, and higher deductibles are just a few of them. If you’ve decided that adding a roommate to your policy just isn’t worth the trouble, take a look at our article on How to get renters insurance discounts to learn about other ways to save.

Renters insurance FAQs

1. Does each roommate need renters insurance?

If your landlord requires you to have renters insurance then, yes, each roommate needs to have renters insurance. If your roommate is a relative or spouse they will be covered under renters insurance.

2. Do I need renters insurance if I live in a dorm?

If you are a college student your personal property may be covered under your parent’s policy so have them check it out to see if you have coverage. Otherwise, yes, just like anywhere else, if your stuff is stolen or destroyed you will have to pay for the cost of replacing all of your stuff out-of-pocket if you don’t have renters insurance. Read our article on Renters insurance for college students to learn more.

3. What is the best renters insurance company?

It’s important to shop around for the best renters insurance company. We’ve compared some companies that we like for you here.

4. What’s the cheapest renters insurance coverage option?

Companies such as Lemonade start their renters insurance as low as $5 a month. Read our article, Cheap renters insurance for more information.

Your renters rights, in your state.

Explore what you need to know.

- Alabama Renters Rights

- Alaska Renters Rights

- Arizona Renters Rights

- Arkansas Renters Rights

- California Renters Rights

- Colorado Renters Rights

- Connecticut Renters Rights

- Delaware Renters Rights

- Florida Renters Rights

- Georgia Renters Rights

- Hawaii Renters Rights

- Idaho Renters Rights

- Illinois Renters Rights

- Indiana Renters Rights

- Iowa Renters Rights

- Kansas Renters Rights

- Kentucky Renters Rights

- Louisiana Renters Rights

- Maine Renters Rights

- Maryland Renters Rights

- Massachusetts Renters Rights

- Michigan Renters Rights

- Minnesota Renters Rights

- Mississippi Renters Rights

- Missouri Renters Rights

- Montana Renters Rights

- Nebraska Renters Rights

- Nevada Renters Rights

- New Hampshire Renters Rights

- New Jersey Renters Rights

- New Mexico Renters Rights

- New York Renters Rights

- North Carolina Renters Rights

- North Dakota Renters Rights

- Ohio Renters Rights

- Oklahoma Renters Rights

- Oregon Renters Rights

- Pennsylvania Renters Rights

- Rhode Island Renters Rights

- South Carolina Renters Rights

- South Dakota Renters Rights

- Tennessee Renters Rights

- Texas Renters Rights

- Utah Renters Rights

- Vermont Renters Rights

- Virginia Renters Rights

- Washington Renters Rights

- West Virginia Renters Rights

- Wisconsin Renters Rights

- Wyoming Renters Rights

- Washington, D.C. Renters Rights